Picture supply: Getty Photographs

Progress shares buying and selling at discounted valuations may be enormous alternatives for buyers. And there’s one specifically that’s catching my eye. The inventory’s gone nowhere for the final 5 years, however the underlying enterprise has performed nicely. So I feel it’s time to take a more in-depth look.

Filtration

The corporate in query is Porvair (LSE:PRV). The agency manufactures filtration tools for the aerospace and laboratory tools industries.

There are a number of causes I like this enterprise, together with:

- Sturdy repeat enterprise.

- Excessive boundaries to entry.

- Resilient income streams.

- Spectacular money conversion.

Let’s take a more in-depth take a look at every of those.

Within the aerospace trade, Porvair’s filters have to get replaced after a sure time. This isn’t non-obligatory – it’s a authorized requirement. With lab tools, loads of the corporate’s merchandise are designed for use as soon as. That results in a gentle stream of repeat gross sales.

Its industries are have excessive regulatory requirements. Whether or not it’s plane, drug improvement or water purity, competing isn’t simple. That makes it tough (or inconceivable) for patrons to modify to various suppliers. And that generates good pricing energy for Porvair.

By way of cyclicality, it’s vital that the agency’s merchandise are sometimes upkeep bills. That makes demand pretty steady, even when firms aren’t increasing.

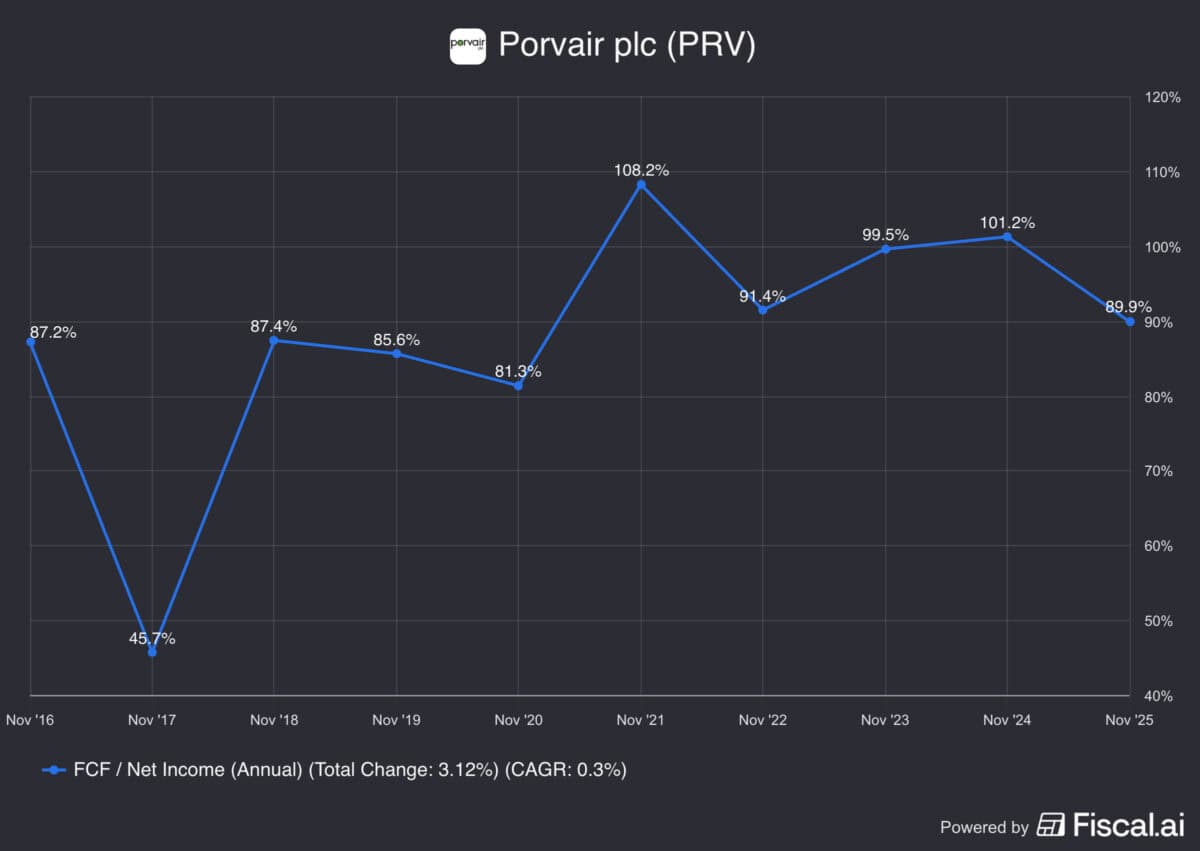

The agency additionally has glorious money conversion metrics. During the last 10 years, it’s persistently turned over 75% of its web earnings into free money.

Useless cash?

This all sounds optimistic, but it surely raises an apparent query. If the enterprise is so good, why has it basically gone nowhere since 2021?

The explanation’s twofold. One’s development – Covid-19 created a surge in demand for lab tools that hasn’t been maintained since. Consequently, Porvair’s needed to take care of larger stock ranges and weaker demand. And this has been a problem for the enterprise.

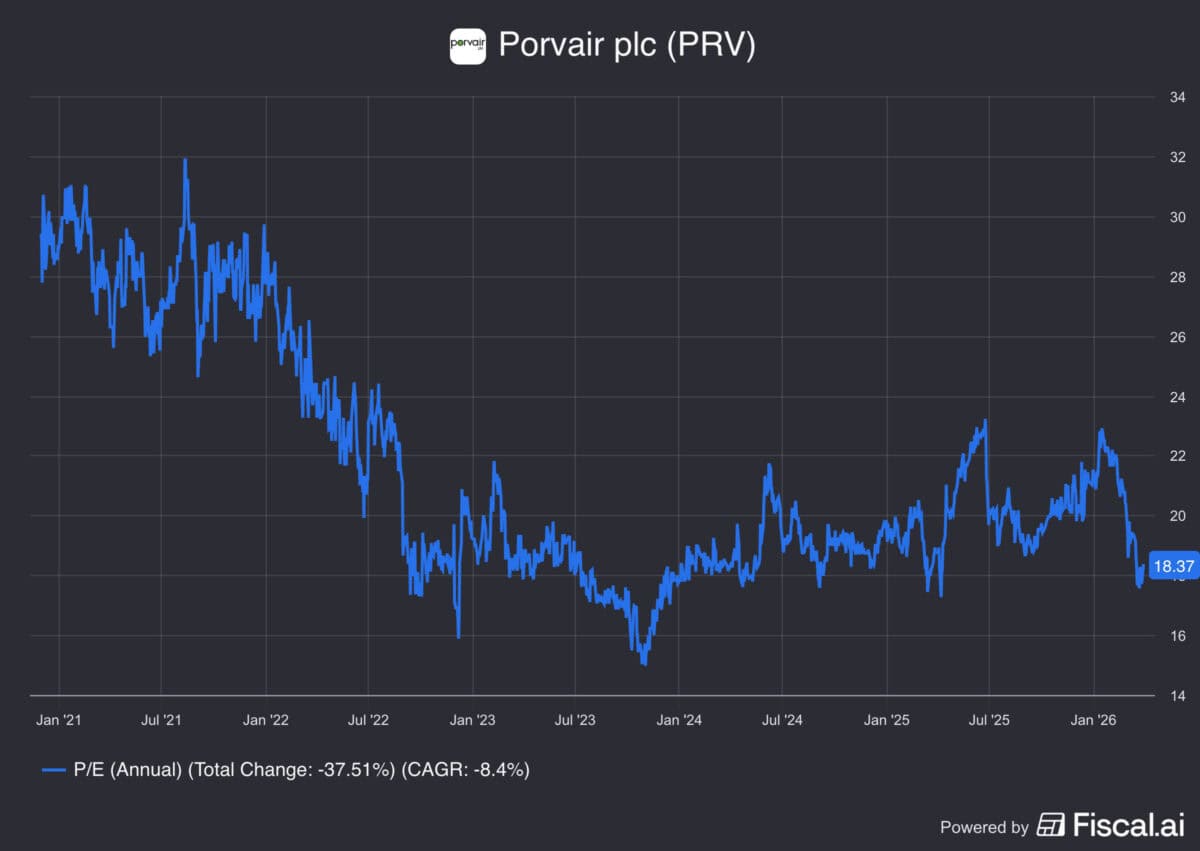

The second’s valuation. 5 years in the past, the inventory was buying and selling at a price-to-earnings (P/E) ratio of 27, which is fairly excessive. As Warren Buffett factors out, it’s doable to pay an excessive amount of even for an impressive enterprise. And I feel this might need been the case in 2021.

Now nonetheless, issues are completely different on each fronts. Demand for lab filters began to recuperate in 2025 after a protracted interval of excessive stock ranges.

On prime of this, the inventory’s now buying and selling at a P/E a number of under 18. So I feel the enterprise has had sufficient time to meet up with the share value.

Dangers and alternatives

Porvair shares are down 15% for the reason that begin of the yr. And a giant cause for that is the continued battle within the Center East. The agency’s comparatively well-protected from cyclical ups and downs, but it surely isn’t proof against a worldwide recession and that’s a danger proper now.

From a long-term perspective although, there’s so much to love in regards to the enterprise. And the present share value seems to be engaging to me. Alternatives like this don’t come round usually, so I feel buyers ought to give this one critical consideration proper now.